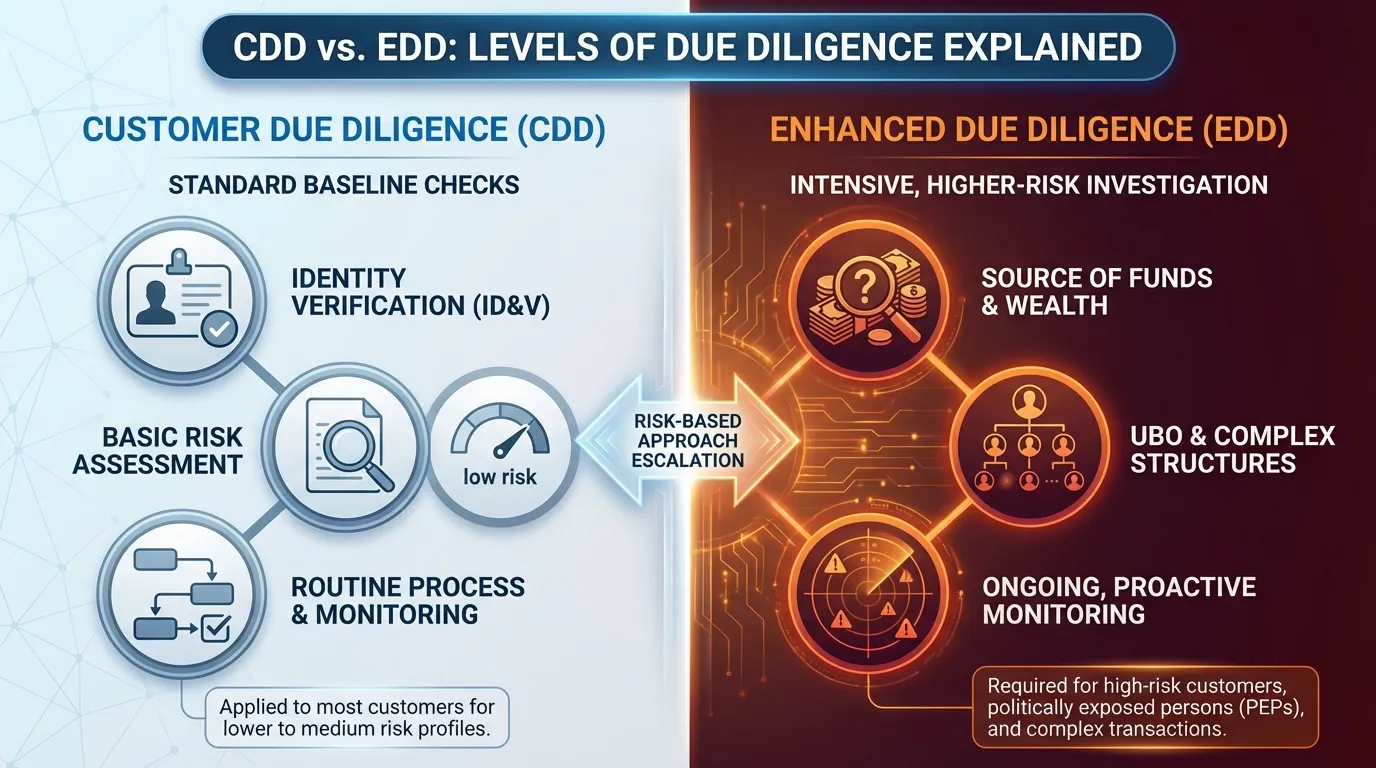

In modern banking and financial systems, customer verification is extremely important. Imagine a person opening a bank account for the first time. The bank asks for identification documents, proof of address, and other personal details. This basic process is called Customer Due Diligence (CDD).

However, if the customer is considered high-risk, the bank conducts a deeper investigation known as Enhanced Due Diligence (EDD). Understanding the difference between CDD and EDD helps explain how financial institutions prevent fraud and illegal activities.

The difference between CDD and EDD is essential in financial compliance and anti-money laundering systems. Banks, financial organizations, and regulators rely on the difference between CDD and EDD to manage customer risk levels. When professionals clearly understand the difference between CDD and EDD, they can apply proper monitoring and security measures. In many cases, the difference between CDD and EDD determines how deeply a financial institution investigates a client before doing business.

Key Difference Between the Both

The main difference between CDD and EDD lies in the level of investigation and risk assessment.

- CDD (Customer Due Diligence) is the standard process used by financial institutions to verify a customer’s identity and understand their financial activities.

- EDD (Enhanced Due Diligence) is a deeper and more detailed investigation used when a customer or transaction is considered high risk.

In simple terms, CDD is the basic verification process, while EDD is an advanced investigation for higher-risk situations.

Why Is Their Difference Necessary to Know for Learners and Experts?

Understanding the difference between CDD and EDD is crucial for professionals working in banking, finance, compliance, and law enforcement. For learners entering the financial sector, knowing the difference between CDD and EDD helps them understand how financial institutions identify suspicious activities and prevent crimes such as money laundering or fraud.

For experts, the difference between CDD and EDD is necessary for implementing proper regulatory compliance. Governments and financial authorities require institutions to apply risk-based monitoring. When professionals understand the difference between CDD and EDD, they can protect financial systems and maintain public trust.

This knowledge is also important for society because strong financial monitoring helps reduce illegal financial activities and promotes transparency in global banking systems.

Pronunciation of Both (US & UK)

| Term | US Pronunciation | UK Pronunciation |

| CDD | /ˌsiː diː ˈdiː/ | /ˌsiː diː ˈdiː/ |

| EDD | /ˌiː diː ˈdiː/ | /ˌiː diː ˈdiː/ |

Now that we know how these terms are pronounced, we can explore their deeper differences and practical applications.

Difference Between the Keywords

1. Level of Investigation

CDD: Basic verification process.

Examples:

- A bank checks a customer’s ID when opening an account.

- A payment platform verifies a user’s identity.

EDD: Detailed and intensive investigation.

Examples:

- A bank investigates a politically exposed person.

- Financial institutions analyze large international transactions.

2. Risk Level

CDD: Applied to low or medium-risk customers.

Examples:

- A regular salary employee opening a savings account.

- A student creating a basic bank account.

EDD: Applied to high-risk customers.

Examples:

- A client involved in international business.

- A customer from a high-risk country.

3. Information Collected

CDD: Collects standard personal details.

Examples:

- Name and address verification.

- National identity documentation.

EDD: Collects deeper financial and background information.

Examples:

- Source of funds investigation.

- Detailed business ownership analysis.

4. Monitoring Frequency

CDD: Periodic monitoring.

Examples:

- Annual account review.

- Basic transaction monitoring.

EDD: Continuous and stricter monitoring.

Examples:

- Daily transaction checks.

- Real-time risk alerts.

5. Complexity

CDD: Simple and routine procedure.

Examples:

- Filling a standard form.

- Uploading identity documents online.

EDD: Complex compliance process.

Examples:

- Investigating business partners.

- Reviewing international financial records.

6. Regulatory Requirement

CDD: Required for all customers.

Examples:

- Opening a bank account.

- Registering for a financial service.

EDD: Required for specific high-risk cases.

Examples:

- Large cross-border transactions.

- Clients with political influence.

7. Cost and Time

CDD: Less costly and faster.

Examples:

- Completed within minutes online.

- Basic document verification.

EDD: Expensive and time-consuming.

Examples:

- Investigative background checks.

- Multi-stage compliance review.

8. Purpose

CDD: To verify customer identity.

Examples:

- Prevent fake accounts.

- Confirm legal identity.

EDD: To identify potential financial crime risks.

Examples:

- Detect money laundering activities.

- Investigate suspicious wealth sources.

9. Depth of Analysis

CDD: Surface-level analysis.

Examples:

- Identity confirmation.

- Basic customer profile.

EDD: Deep financial and behavioral analysis.

Examples:

- Investigation of financial history.

- Monitoring of unusual transactions.

10. Documentation

CDD: Requires standard documents.

Examples:

- Passport or national ID.

- Proof of residence.

EDD: Requires extended documentation.

Examples:

- Tax records.

- Business ownership documents.

Nature and Behaviour of Both

CDD has a preventive and foundational nature. Its main purpose is to identify customers and establish basic trust between financial institutions and clients.

EDD has a protective and investigative nature. It is designed to detect hidden risks and suspicious financial behavior. While CDD focuses on identification, EDD focuses on deeper investigation and risk analysis.

Why People Are Confused About Their Use?

| Feature | CDD | EDD | Similarity |

| Purpose | Basic customer verification | Advanced risk investigation | Both verify customers |

| Risk Level | Low or medium | High | Used in financial compliance |

| Depth | Standard checks | Detailed checks | Prevent financial crime |

| Usage | Common for all customers | Only for risky cases | Used in banking systems |

Many people are confused because both processes are part of financial verification systems.

Which Is Better in What Situation?

CDD is better for normal banking situations where customers pose little risk. It allows financial institutions to verify identity quickly and efficiently. Most everyday customers only go through CDD because their activities are simple and transparent.

EDD is better when a customer or transaction is considered high risk. Financial institutions must investigate further to ensure that illegal activities such as money laundering or fraud are not occurring. In these cases, deeper scrutiny is necessary.

How the Keywords Are Used in Metaphors and Similes

In professional discussions, these terms can appear metaphorically.

Examples:

- “Good research works like CDD, verifying facts before making conclusions.”

- “Investigative journalism often functions like EDD, examining deeper layers of truth.”

Connotative Meaning

CDD

- Positive/Neutral: Responsible identity verification.

Example: “The bank completed CDD before opening the account.”

EDD

- Neutral: Advanced investigation process.

Example: “The company conducted EDD on high-risk clients.”

Idioms or Proverbs Related to the Words

Although no traditional idioms exist, similar expressions are used.

Examples:

- “Do your due diligence.” – Meaning investigate carefully.

- “Look beneath the surface.” – Meaning deeper analysis like EDD.

Works in Literature Related to the Topic

- Money Laundering: A Guide for Criminal Investigators – John Madinger (2006) – Finance/Crime nonfiction

- The Laundrymen – Jeffery Robinson (1995) – Financial crime investigation

- Global Financial Crime – Donato Masciandaro (2007) – Economic analysis

Movies Related to Financial Investigation

- The Wolf of Wall Street – 2013 – USA

- The Big Short – 2015 – USA

- Margin Call – 2011 – USA

Frequently Asked Questions

1. What does CDD mean?

CDD stands for Customer Due Diligence, a basic process used to verify a customer’s identity.

2. What does EDD mean?

EDD stands for Enhanced Due Diligence, which involves deeper investigation of high-risk clients.

3. When is EDD required?

EDD is required when a client or transaction presents a higher risk of financial crime.

4. Is CDD mandatory?

Yes, most financial institutions must perform CDD for all customers.

5. Can a customer move from CDD to EDD?

Yes, if the risk level increases, institutions may apply EDD procedures.

How Both Are Useful for Surroundings

CDD and EDD help maintain financial transparency and security in society. They protect financial systems from fraud, corruption, and money laundering. These processes also help governments enforce financial regulations and maintain trust in banking institutions.

Final Words for Both

CDD and EDD are essential components of financial risk management. While CDD forms the foundation of customer verification, EDD provides deeper protection against financial crimes. Together, they ensure the integrity of financial systems.

Conclusion

The difference between CDD and EDD lies mainly in the depth of investigation and the level of risk involved. CDD focuses on basic identity verification for regular customers, while EDD is used for high-risk individuals or transactions requiring deeper scrutiny.

Understanding the difference between CDD and EDD helps professionals apply proper compliance procedures and ensures financial institutions operate safely. In today’s global financial environment, these processes are vital tools for preventing illegal financial activities. By recognizing the difference between CDD and EDD, learners and experts can better understand how modern financial systems protect businesses, governments, and society.

.

I am a professional blogger and content writer specializing in synonyms. With a strong focus on research-based writing and clear communication, I creates high-quality content designed to inform, educate, and add long-term value for readers.I am committed to maintaining accuracy, consistency, and professionalism across all published work.